Finance isn’t just about wealth or Wall Street — it’s a part of your daily life. From grabbing coffee to planning a wedding, money touches almost every decision we make. Learning how to manage your finances is one of the most empowering steps you can take toward a more stable, confident, and fulfilling life. Whether you're saving for a rainy day, trying to understand your taxes, or planning for retirement, the right financial knowledge puts you in control of your future.

Personal Finance & Budgeting

Money doesn’t come with instructions — but creating a budget is the closest thing to one. At its core, budgeting is about awareness. It's how you see where your money goes, how you plan for what’s ahead, and how you make room for what matters.

A popular starting point is the 50/30/20 rule, which breaks down your after-tax income into:

-

50% for needs (rent, groceries, transportation)

-

30% for wants (entertainment, dining out)

-

20% for savings or debt repayment

Let’s say you earn $3,500 each month. A basic breakdown would look like this:

-

$1,750 for needs

-

$1,050 for wants

-

$700 for savings or paying down loans

But budgeting isn’t one-size-fits-all. Some prefer zero-based budgeting, where every dollar is assigned a job — while others use the envelope method, physically or digitally dividing cash into categories to prevent overspending.

🔍 Mini Scenario:

You’ve got $1,200 left after paying fixed bills this month. You want to save for a trip, pay off part of your credit card, and still enjoy a night out or two. How do you decide what goes where?

That’s where tools like our [Budget Calculator] and [Savings Calculator] can help — giving you a clearer picture and helping you stay on track without guesswork.

Ultimately, budgeting isn’t about restriction. It’s about choice. Knowing where your money is going lets you decide where you want it to go next.

Loans, Debt, and Investments

Interest can work for you or against you — depending on which side of the equation you're on. When you borrow money, interest adds to the cost. When you invest or save, interest helps your money grow. That’s why understanding how interest works is a major step toward making smarter financial decisions.

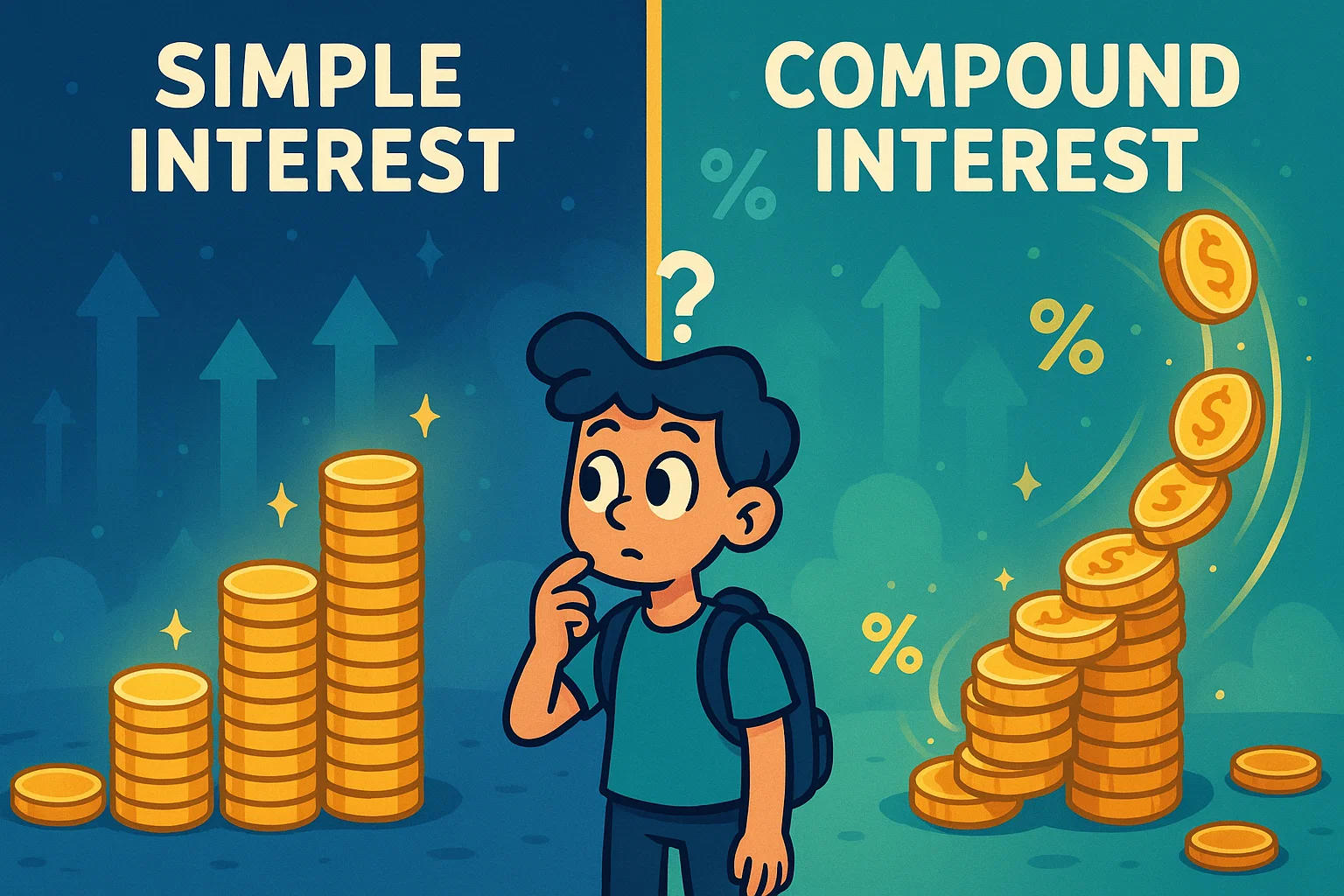

Simple vs. Compound Interest

Not all interest is created equal — and knowing the difference can help you make smarter choices whether you’re borrowing money or growing your savings.

Simple interest is straightforward: you earn or pay interest only on the original amount, also known as the principal. For example, if you borrow 1,000ata550 each year — no more, no less. It’s predictable, and that makes it easy to plan for. You can see exactly how it works using our Simple Interest Calculator, whether you're checking a loan or comparing fixed savings options.

Compound interest, on the other hand, builds over time — not just on the principal, but also on the interest that’s already been added. So if you invest 1,000at550 each year. Over five years, your money grows to about $1,276. That’s the power of compounding. Try our Compound Interest Calculator to see how your savings could grow.

Taking Out a Loan

Imagine you borrow 10,000foracarloanwith710,000 plus a bit more— but depending on the terms, your total repayment could be $11,800 or more.

That’s why estimating your monthly payments before taking out a loan is so important.

You can try it with our Loan Calculator or Interest Calculator to explore:

-

Total interest over time

-

Monthly payments based on loan length

-

How a slightly lower rate can save you hundreds (or even thousands)

Investing Made Simple

Investing doesn’t have to mean picking stocks or following the market every day. Index funds, retirement accounts, and employer-sponsored plans like a 401(k) or IRA are all ways to use compound growth to your advantage. These accounts come with tax benefits and long-term growth potential, making them smart choices for retirement planning.

Not sure how much to contribute, or how much you'll have by retirement? Tools like our 401(k) Calculator and IRA Calculator can help you estimate your future balance based on your income, contributions, and timeline.

The earlier you start, the more time your money has to grow. Even small, regular investments can add up — consistency matters more than timing the market.

Tax Basics and Financial Literacy

Let’s be honest — taxes can feel like a black box. You earn money, some of it disappears from your paycheck, and once a year you hope for a refund. But once you understand how taxes actually work, things start to make a lot more sense — and a lot less stressful.

Most countries use a progressive tax system, which means you’re taxed in chunks, not all at once. If you make $50,000 a year, only part of that is taxed at higher rates — not the whole thing. It’s a common misunderstanding, but it can affect how you plan your finances.

If you’re curious about what you’ll owe or what a raise might really look like after taxes, tools like our Income Tax Calculator and Take-Home Pay Calculator give you a clear picture — no guesswork, no surprises.

Then there’s the question of deductions and credits. They sound technical, but they’re just ways to lower your tax bill. A deduction reduces how much of your income gets taxed. A credit takes money directly off your tax total. And if you’re self-employed? You’ve got a few extra steps to take, but our Self-Employment Tax Calculator can guide you through it.

Financial literacy around taxes empowers you to plan better — not just for April, but for your entire financial life.

Your Money, Your Control

Managing money doesn’t require a finance degree — just curiosity, a bit of knowledge, and the right tools. Whether you're looking to pay off debt, plan a vacation, or understand how interest works, financial literacy helps you make smarter choices with lasting impact.

At AllTheTools.com, we offer simple, effective calculators to guide your decisions — so you can focus on what really matters: building the life you want.